Title : Lessons on Inflation from the Past

link : Lessons on Inflation from the Past

Lessons on Inflation from the Past

Lessons on Inflation from the Past

September 26, 2020

This article examines two inflationary experiences in the past in an attempt to predict the likely outcome of today’s monetary policies. The German hyperinflation of 1923 demonstrated that it took surprisingly little monetary inflation to collapse the purchasing power of the paper mark. This is relevant to the fate of the “whatever it takes” inflationary policies of today’s governments and their central banks. The management of John Law’s Mississippi bubble, when he used paper money to rig the market is precisely what central bank policy is aimed at achieving today. By binding the fate of the currency to that of financial assets, as John Law proved, it is the currency that is destroyed.

Introduction

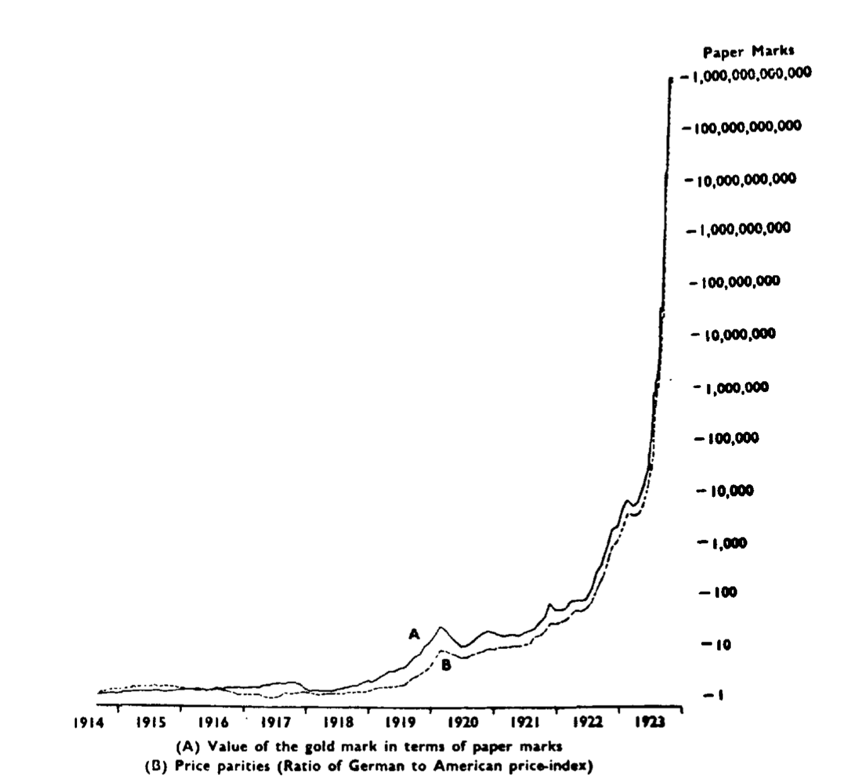

At the outset, I shall make a point about the relevance of the chart below, a screengrab from Constantino Bresciani-Turroni’s The Economics of Inflation[i], which has been frequently reproduced and will be familiar to many who have read about Germany’s post-First World War inflation.

Looking at the progress of the collapse of the paper mark from its parity with the gold mark, we can take a punt on where the dollar might be today on this scale. The dollar has lost 98.2% of its purchasing power since the failure of the London gold pool in the late 1960s. That puts the dollar at 56 on the chart, which is approximately the equivalent of Germany’s paper mark valuation relative to gold in the first half of 1922. If it follows the same course as the paper mark, in five- or six-months’ time it will be 100 and in ten- or twelve-months about 12,000. Instead of the paper mark’s original pre-1914 parity to the gold mark, the dollar started at $35 to the ounce, so the gold price in dollars would be $1960, $3,500 and $42,000 respectively. The final price at which the German inflation was stopped on 20 November 1923 when it was fixed to the rentenmark at a trillion to one would be the equivalent today of $35 trillion to the ounce.[ii]

BALEAF Women’s 3...Buy New $29.99(as of 06:11 EDT - Details)

BALEAF Women’s 3...Buy New $29.99(as of 06:11 EDT - Details) Playing around with figures like these is not a replacement for sound reasoning, but it does impart an interesting perspective. A better understanding of the possible demise of the unbacked dollar is not to think of the numbers of dollars per ounce of gold rising or gold potentially hitting $42,000 within a year, a seemingly ridiculous number, but to think of gold as being broadly stable while the dollar loses its purchasing power. The presentation of an impossibly steep and accelerating uptrend is less believable than a collapsing one. Furthermore, the commonality of the paper mark and the dollar is that they were and are unbacked state-issued currencies liable to the same influences, a fact the consequences of which are becoming increasingly apparent.

Playing around with figures like these is not a replacement for sound reasoning, but it does impart an interesting perspective. A better understanding of the possible demise of the unbacked dollar is not to think of the numbers of dollars per ounce of gold rising or gold potentially hitting $42,000 within a year, a seemingly ridiculous number, but to think of gold as being broadly stable while the dollar loses its purchasing power. The presentation of an impossibly steep and accelerating uptrend is less believable than a collapsing one. Furthermore, the commonality of the paper mark and the dollar is that they were and are unbacked state-issued currencies liable to the same influences, a fact the consequences of which are becoming increasingly apparent.

Germany’s 1920s hyperinflation

For the paper mark it all started in 1905, when a German economist and leader of the Chartalist movement, Georg Knapp, published a book whose title translated as the State Theory of Money. Thus encouraged, under the direction of Bismarck the Prussian administration financed the military build-up to the war to end all wars by utilising the state’s seigniorage. And when Germany lost, any thoughts of raiding the wealth of the vanquished came to nought. Instead, it was Germany that faced reparations and a post-war crisis. Just as the Fed is responding to the covid crisis today, the answer was to print money. Monetary inflation became the principal source of government finance, just as it is now in America and elsewhere.

There is hardly an economist today who does not condemn the Reichsbank for its inflationary policies. Yet they are supportive of similar monetary policies by the Fed, the European Central Bank, the Bank of Japan and the Bank of England. We should compare the stewardship of Rudolf Havenstein at the Reichsbank with that of Jay Powell, who after reducing interest rates the previous week, on 23 March issued an FOMC statement promising an inflationary policy of “whatever it takes”. And Rishi Sunak, the British Chancellor, used the phrase multiple times in his emergency budget.

But there is a difference. Today, alternatives to inflationism are never discussed amongst policy makers, who are like a blind cult believing entirely, with only minor variations, that monetary inflation is the cure for all economic ills. At least in Germany, the actions of the government were the subject of wider debate both in Germany and without, even though the answers were mostly ill-informed.

Part of the problem was the quantity theory of money was dismissed in a confusion between cause and effect. As Bresciani-Turroni put it, a great number of writers and German politicians thought that government deficits and paper inflation were not the cause, but the consequence of the external depreciation of the mark. A financier, politician and one of the leading German economists at the time, Karl Helfferich put it this way:

“The increase of the circulation has not preceded the rise of prices and the depreciation of the exchange, but it followed slowly and at great distance. The circulation increased from May 1921 to the end of January 1923 by 23 times; it is not possible that this increase had caused the rise in the prices of imported goods and of the dollar, which in that period increased by 344 times.[iii]”

It is a valid and important point, but not in the way Helfferich thought. The disparity between the increase in the money quantity and the increase in the general level of prices should be noted by observers today. Crucially, it did not require hyperinflation of the money supply to cause a hyperinflation of prices, a point we address later.

As well as dealing with the post-war economy and the capital dislocation that needed to be corrected, there was the burden of reparations. Many blamed the collapse of the paper mark on the latter, which is an inadequate explanation, when the Austrian crown, the Hungarian crown, the Russian rouble and the Polish mark all collapsed at roughly the same time.

Having resorted to monetary inflation as the means of marginal finance it rapidly became the principal source of government revenue. The German authorities then observed a dislocation between the increase in the quantity of money and the effect on its purchasing power, as described by Helfferich. It was taken as evidence against the quantity theory, as expounded by David Ricardo a century before, and upon which Peel’s Bank Charter Act of 1844 in England was based. Clearly, the dismissal of the quantity theory paved the way for more inflationary financing in 1920s Germany in the manner of today’s monetary planning. It led to the observation that the money supply was insufficient for an economy faced with rapidly escalating prices for imported goods. Blood Sweat And Gears ...Buy New $21.99(as of 06:11 EDT - Details)

Blood Sweat And Gears ...Buy New $21.99(as of 06:11 EDT - Details)

The disparity between increases in the money supply in Germany and the effect on the paper mark’s purchasing power was so great that the accuracy of the underlying numbers does not matter. But today, while we can presumably rely on monetary statistics being reasonably accurate, the statistics that reflect the effect on prices are not. Today’s suppression of increases in the general price level simply disqualifies any statistical analysis, and in that sense, Helfferich’s observation is a more honest appraisal than those of today’s monetary planners.

On the surface, his deduction appeared to have some merit. He goes on to say,

“The depreciation of the German mark in terms of foreign currencies was caused by the excessive burdens thrust on to Germany and by the policy of violence adopted by France; the increase of the prices of all imported goods was caused by the depreciation of the exchanges; then followed the general increase of internal prices and of wages, the increased need for means of circulation on the part of the public and of the State, greater demands on the Reichsbank by private business and the State and the increase of the paper mark issues. Contrary to the widely held conception, not inflation but the depredation of the mark was the beginning of this chain of cause and effect; inflation is not the cause of the increase of prices and of the depreciation of the mark; but the depreciation of the mark is the cause of the increase of prices and of the paper mark issues. The decomposition of the German monetary system has been the primary and decisive cause of the financial collapse.”[iv]

The starting point in this logic is it is never the government’s fault but always the fault of external factors and markets. And doubtless, as the dollar declines in the foreign exchanges over the coming months and commodity prices rise, we shall continue to see similar arguments embedded in future FOMC statements.

The error common to both is to misunderstand the underlying subjectivity of money. Money takes its value from the marginal value placed upon it relative to owning goods. If money is widely regarded as sound, an economising man is happy to hold a reserve of it, only exchanging it for goods and services when they are needed. This is the most important quality of metallic money, to which people have always returned when government money fails.

A further benefit, which state currencies lack, is that gold and silver as money are accepted everywhere, having the same values in New York, London, and Mumbai. With the exception of cross-border trade, investment, and perhaps longer-term strategic considerations, government currencies are generally restricted to national boundaries. Paper currencies are therefore vulnerable to changes in demand in the foreign exchanges in a way gold and silver are not; if the foreigners don’t like your currency, they will reduce their exposure by selling it, irrespective of fundamental considerations.

In a currency collapse, the foreign exchanges are often the first to be blamed, as a press cutting from Germany towards the end of 1922 illustrates:

“Since the summer of 1921 the foreign exchange rate has lost all connection with the internal inflation. The increase of the floating debt, which represents the creation by the State of new purchasing-power, follows at some distance the depreciation of the mark. Furthermore, the level of internal prices is not determined by the paper inflation or credit inflation, but exclusively by the depreciation of the mark in terms of foreign currencies. To tell the truth, the astonishing thing is not the great quantity but the small quantity of money which circulates in Germany, a quantity extraordinarily small from a relative point of view; even more surprising is it that the floating debt has not increased much more rapidly.[v]”

Blaming a falling currency on foreign influences is the oldest excuse in the fiat book, but generally, foreigners who do not have much attachment to a national currency are only the first to sell. Initially, domestic users notice that prices have generally risen and that their income and savings buy less. It is a cause for complaint instead of a reasoned assessment, and of the logic employed in the press cutting above. And despite the evidence that it is the currency losing purchasing power instead of prices rising, the purchasing power can fall substantially before a currency’s users abandon it altogether. Cycling gloves (Black ...Buy New $16.95(as of 06:11 EDT - Details)

Cycling gloves (Black ...Buy New $16.95(as of 06:11 EDT - Details)

Given upcoming events, we can see a similar trend for today’s paper money, particularly when represented by the American dollar. The first covid wave was assumed to be a one-off, hitting the American economy but to be followed by a rapid return to normal — the V-shaped recovery. Everywhere the official story was the same, that following lockdowns the economy, wherever it was, would return to normality. But it drove the US budget deficit to over $3.3 trillion in the fiscal year just ending, up from a previously forecast trillion or so.[vi] The Federal deficit is already one hundred per cent of Federal tax revenues.

Now we face a second covid wave, which will require more money-printing. The US Government budget deficit in the next fiscal year will again exceed revenues by a substantial margin. From last March, it has been in the position the German government faced in the early 1920s: monetary inflation has become the dominant source of government funding over tax revenue.

The slide in global cross-border trade, which is the consequence of the imposition of trade tariffs between America and China, comes at the end of a decade-long period of bank credit expansion, replicating the fragile position in America at the end of the roaring twenties. The stock market and economic collapses that followed had limited inflationary effects at the price level only due to a working gold standard; but even that could not withstand the political consequences of the depression, leading to a dollar devaluation in January 1934. This time, there is no check for the dollar, which is doubly afflicted by coronavirus lockdowns.

In Germany, the collapse of the paper mark ended by being stabilised at the rate of a trillion to one gold marks on 20 November 1923, the equivalent of 4.2 trillion to the US dollar. The paper mark was then replaced by a new unit, the rentenmark which was simply given the value of the gold mark. This arrangement only became legal on 11 October 1924. The success of the stabilisation, despite an inflation of the rentenmark — the quantity increasing from 501 million on 30 November 1923 to 1,803 million by the following July — has confused economists ever since.

Students of the Austrian school, and particularly of the writings of Ludwig von Mises should deduce that after the final flight out of money into goods, the emergence of a new money requires its users to accumulate a reserve of it. All that was required was a growing acceptance that the rentenmark would stick. The increase in cash and savings balances in the economy absorbed the increased inflation of the rentenmark with the result that consumer prices remained broadly stable.

If the stabilisation arrangement had been introduced before foreigners, businesses and the wider public had not discarded the paper mark entirely, the stabilisation would have failed. Those who think a German-style inflationary collapse today can be avoided by an early currency reset with a different form of fiat should take note.

The comparison with John Law’s crisis in 1720

The collapse of the paper mark is not the sole representation of how a government currency loses its facility. The advantage of its comparison with today is that a substantial cache of books, records and statistics exist on the subject, prompting economic historians to use it as a template for all the other hyperinflations of fiat money recorded since.

The economic history of John Law’s experiment in France in not so blessed in this regard. Exactly 300 years ago, his Mississippi bubble deflated, taking his currency, the livre, down with it. But to understand the relevance to the situation today, we must first delve into the facts behind his scheme.

The death of Louis XIV in 1715 left France’s state finances (which were the royal finances) insolvent. The royal debts were three billion livres, annual income 145 million, and expenditure 142 million. That meant only three million livres were available to pay the 220 million interest on the debt, and consequently the debt traded at a discount of as much as 80% of face value.[vii]

Following Louis XIV’s death, the Duke of Orleans had been appointed Regent to the seven-year old Louis XV, and so had to find a solution to the royal finances. The earlier attempt in 1713 was the often tried and repeatedly failed expedient of recoining the currency, depreciating it by one-fifth. The result was as one might expect: the short-term gain in state revenue was at the expense of the French economy by taxing it 20%. Furthermore, the Controller General of Finances foolishly announced the intention of further debasements of the coinage with a view to raising funds. This bizarre plan was announced in advance as an attempt to somehow stimulate the economy, but the effect was to increase hoarding of the existing coinage instead. Tough Headwear Helmet ...Buy New $9.95(as of 06:11 EDT - Details)

Tough Headwear Helmet ...Buy New $9.95(as of 06:11 EDT - Details)

At about this time, John Law presented himself at court and offered his considered solution to the Regent. He diagnosed France’s problem as there being insufficient money in circulation, restricted by it being only gold and silver. He recommended the addition of a paper currency, such as that in Britain and Holland, and its use to extend credit.[viii]

Banknotes did not previously exist in France, all payments being made in specie, and Law persuaded the Regent of the circulatory benefits of paper money. He requested the Regent’s permission to establish a bank which would manage the royal revenues and issue banknotes backed by them as well as notes secured on property. These notes could be used as a loan from the bank to the king at 3% interest instead of the 7½% currently being paid on billets d’etat.

On 5 May 1716 he gained permission to establish Banque Generale as a private bank and to issue banknotes. Law succeeded in persuading the public to swap specie for his banknotes. He was so successful that after only eleven months, in April 1717 it was decreed that taxes and revenues of the state could be paid in banknotes, of which Law was the only issuer.

Law could now capitalise his bank. Besides his own money, this was done mostly with billets d’etat, in the books at their face value but obtained at a discount of 70% or so. He used public anticipation of future currency debasement to encourage the public to swap metallic money for his notes, which he guaranteed were repayable in coins that had the silver content at the time of the note issue. Law’s banknotes became an escape route for the general public from further debasement of silver coins.

The banknotes rose to a fifteen per cent nominal premium over coins within a year. The bank was exempt from taxes, and by decree foreigners were guaranteed their deposits in the case of war. The bank could open deposit accounts, loan money, arrange for transfers between accounts, discount bills and write letters of credit. Law’s banknotes could be used to settle taxes. There was no limitation placed on the total number of banknotes issued.[ix]

Money that had been hoarded for fear of further debasement was liberated by the premium on Law’s banknotes, and the improved circulation of money rapidly benefited the economy. Other private banks and moneylenders used Law’s banknotes as the basis of extending credit.[x] This success meant his credibility with the Regent, the French establishment, and the commercial community was secured.

The use of his banknotes to settle taxes gave the bank the status of a modern note-issuing central bank. The expansion of circulating money stimulated trade, particularly given the banknotes’ convenience compared with using coin. It is worth noting that the earliest stages of monetary inflation usually produce the most beneficial effects, and this combined with Law’s apparent financial and economic expertise, particularly measured against the ineptitude of the Controller-General of Finances, gave the economy a much-needed boost.

It is worth noting that at this stage, there was no material inflation of the currency, banknotes being issued only against coins. However (and this appears to have generally escaped economic historians) it was clear that a loan business was facilitated on the back of Law’s paper money, which inflated the quantity of bank credit in the economy.

Law could now turn his attention to raising asset prices to pay down the royal debts, to enhance the public’s riches, and thereby his own wealth and that of his bank.

The Mississippi connection

The Regent was understandably impressed by Banque Générale’s apparent success at issuing paper currency and rejuvenating the economy. The bank was being run on prudent lines, with banknotes being exchanged only for specie, and the quantity of what today would be called narrow money had not expanded materially beyond the release of hoarded specie. But Law had a problem: the note issue and the fact the bank had been capitalised on a mixture of partial subscriptions and billets d’etats at face value meant the bank had insufficient capital and profits to achieve its ultimate objective, which was to reduce the royal debts and the interest rates that applied to them.

Consequently, Law developed a plan to increase the bank’s assets as well as those under its indirect control. In August 1717, Law had requested of the Regent and was granted a trading and tax-raising monopoly over the French territory of Louisiana and the other French dependencies accessed by the Mississippi River, the existing trading lease having lapsed. A major attraction was supposed to be precious metals as well as the tobacco trade.

The Mississippi venture’s corporate title was Compaigne de la Louisiane ou d’Occident, but ever since has been commonly referred to as the Mississippi venture. For nearly two years, Law kept the project on hold while he established his bank. The shares languished at a discount to their nominal price of 500 livres, and what was needed was a scheme of arrangement to beef up the both the bank and the company.

As a first step, in the summer of 1719 he acquired three other companies to merge with the Mississippi venture. These had exclusive trading rights to China, the East Indies and Africa, which effectively gave Law’s Mississippi company a monopoly on all France’s foreign trade. To pay off these companies’ debts and to build the ships required for transport, Law proposed a share issue of 50,000 shares at 500 livres per share, 10% payable on application. By the time legal permissions were granted, the shares stood at 650 livres, making the new shares worth three times their subscription price in their partly paid form.

Law’s earlier success with his banknote issue, and the contribution made to improving the French economy, coupled with his ability to enhance the share price by issuing bank notes, were a guarantee that his scheme would be spectacularly profitable for anyone lucky enough to have a subscription accepted.

The bank was re-authorised as a public institution and renamed Banque Royale in December 1718. At the same time, the Regent authorised the further issue of up to a billion livres of notes, which was achieved by the end of 1719. While it had been the Banque Generale, notes had only been issued in return for specie to the extent of 60 million livres, but this new inflationary issue was entirely different. While it is impossible at this distance to forensically track the course of this money, we can be certain that it was used to manage the share price of the Mississippi venture, and it fuelled much of the public’s panic buying of shares that year.

But it was not only the printing of money to push the share price that fuelled the bubble. Law’s skills as a promoter took its inflation to a new level, with further issues of 50,000 shares approved in the summer of 1719 and executed as rights issues that autumn. Existing shareholders were offered the opportunity to subscribe for one share for every four old shares held, to be partly paid with an initial payment of 50 livres, the next payment deferred for over a month. These could be sold for an immediate profit, while providing a low-price entry point for new investors.

The expansion of the banknote issue without an offsetting acquisition of specie was used by Law to assemble and finance a total monopoly of France’s foreign trade. As well as this monetary expansion, we can be sure that private banks and moneylenders used it as a base to expand credit. We know this to be the case from court documents in London when Richard Cantillon in 1720 successfully sued English clients in the Court of Exchequer for £50,000 owed to him (about £18 million today), despite having already sold the Mississippi shares as soon as they were deposited as collateral.

It seems obvious to us that to give to one man both the monopoly of the note issue and monopolies on trade, and then for him to use the notes to create wealth out of thin air is extraordinarily dangerous. It seems equally obvious that such an arrangement was certain to collapse when the excitement died down and investors on balance sought to encash their profits.

It seems less obvious to us today that the principal elements of Law’s monopolies exist in modern government finances, which use paper money to inflate assets providing their electorates with the illusion of wealth.[xi] The difference is not in the methods employed, but the gradualness of today’s asset inflation, and the claim by the state that it is acting in the public interest, rather than one individual making the same claim on the state’s behalf.

Meanwhile, the Mississippi venture share price had continued rising, and by the end of 1719 it stood at 10,000 livres. Increasing pressure from share sales by people who sought to take profits had to be discouraged. The announcement of a 200 livres dividend per share was undoubtedly with that in mind, to be paid, like in any Ponzi scheme, not out of earnings but out of capital subscriptions. The price finally peaked at 11,000 livres on 8th January 1720.

By late-1719, Law had found it increasingly difficult to sustain the bubble. The banknote issues continued. In late-February 1720, the Mississippi Company and the Banque Royale merged. Afterwards, the shares began their precipitous fall, and by May, Law lost his position as Controller-General and was demoted. By the end of October that year, the shares had fallen to 3,200 livres, and a large portion of them had faced further unpaid calls throughout that year.

The year 1719 saw monetary inflation take off, directly fuelling asset prices. The decline of the Mississippi share price the following year was not as sharp as might otherwise have been expected, but against that must be put the fall in the paper livre’s purchasing power, particularly in the later months. The exchange rate against English sterling fell from nine old pence to 2 ½ pence in September 1720, most of that fall occurring after April as the price effect of the previous year’s inflation worked its way through into the exchange rates.

In the last three months of 1720 there was no sterling price quoted for paper livres, indicating they had become worthless.

The relevance to today

John Law’s ramping of a single financial asset by monetary inflation correlates with the Fed’s monetary policy today. The material differences are the suppression of interest rates, and therefore the market costs of government funding, and the far wider range of financial assets being inflated on the back of government bonds. The importance of maintaining financial asset prices is not only Fed policy, but it is increasingly realised that it is a policy that cannot be allowed to fail.

To the extent that other central banks are suppressing yields on their government bonds, this policy extends beyond America. This time, the John Law strategy has gone truly global, with the consequence that the future of fiat currencies is tied to the perpetuation of current financial bubbles.

In this regard it is interesting to note that the most astute banker in John Law’s time, Richard Cantillon, never played Law’s game on the bull tack. He made his first fortune extending credit to others for the purchase of John Law’s stock, which as collateral he promptly sold. Subsequently, he sued for the return of the loans to those who refused to pay up, thereby getting two bites of the cherry. His second fortune was shorting Law’s scheme in 1719, not by selling shares in the scheme, but by selling the currency for foreign exchange. In other words, he calculated that when the scheme failed, it would be the currency that collapsed more than the shares. He was right.

Conclusion

The two empirical models by which we can judge the collapse of a fiat currency offer food for thought in our current situation. The policy of deliberately rigging financial markets replicates that of John Law’s scheme, suggesting the collapse of currencies will be tightly bound to the end of the government bond bubble. Today’s bubbles in financial assets are sustained by equally artificial means, even more transparent than Law’s market rigging — quantitative easing, suppressed and negative interest rates etc., to which we can add the manipulation of price inflation statistics.

The German experience in the early 1920s showed how it did not take as much monetary inflation as monetarists might think to collapse a currency. Karl Helfferich’s quote about the relationship between the 23 times increase in the money quantity while the number of paper marks to the dollar increased 344 times gives us an important perspective: it will not require a hyperinflation of the money suppy to destroy paper currencies today.

A fundamental difference is that the greatest sinner, if not on scale but likely effect, is the Fed in its puffery of the dollar, everyone else’s reserve currency. And unlike Germany a century ago and unlike France three centuries ago, there is no foreign currency against which to measure the dollar’s decline, except perhaps in the short run, because all central banks follow similar inflationary policies with their fiat currencies.

In the past a suitable foreign currency was fully exchangeable into silver or gold, so the decline and collapse could only be measured accordingly. It also means that it will be impossible for businesses to bypass the currency collapse by referencing prices to other currencies, being all similarly fiat. Many businesses in Germany survived the paper mark collapse in this way, but their modern equivalents will not have this option.

The final collapse of a currency is always a flight out of government fiat currency into goods. That can be the only outcome from the continuation of current macroeconomic policies. But above all, it would be a mistake to think it cannot happen, nor that it will be a long process giving us all plenty of time to plan. The final flight out of paper marks took approximately six months. Law’s scheme took slightly longer to destroy his livre. These should be our reference points.

—

[i] First published in Italian in 1931, and in English in 1937.

[ii] For ease of reference, a milliard was the term for today’s billion, a billion was the term for today’s trillion, and a trillion was a million of today’s trillion.

[iii] Bresciani-Turroni, pp. 44, translated from Helfferich’s Das Geld (1923)

[iv] Ibid. pp. 45

[v] Ibid pp. 45

[vi] Latest Congressional Budget Office estimate

[vii] Earl J Hamilton, The Political Economy of France at the time of John Law (History of Political Economy – 1969)

[viii] Law appears to have failed to emphasise sufficiently the sheet-anchor guaranteeing British banknotes through conversion into silver on demand.

[ix] See Early Speculative Bubbles and Increases in the Supply of Money, by Doug French (Mises Institute)

[x] The most famous of these private bankers was Richard Cantillon, famous for his essay on economics and the Cantillon effect.

[xi] Alan Greenspan made it clear that a rising stockmarket was an essential objective of monetary policy to spread a beneficial wealth effect, when he was Fed chairman.

Thus Article Lessons on Inflation from the Past

You are now reading the article Lessons on Inflation from the Past with the link address https://polennews.blogspot.com/2020/09/lessons-on-inflation-from-past.html

0 Response to "Lessons on Inflation from the Past"

Post a Comment